46 / 84

46 / 84

ECONOMIC REPORT

2016

46

6. Supply Chain

With the upstream sector experiencing one of its most challenging periods in history, there is considerable ongoing

impact on businesses right across the supply chain. While 12 months ago many companies still had a backlog of

orders to service, the reality is that many now face an emptying order book and are having to compete fiercely for

available business. Some have been able to do so successfully and have grown their businesses this year, others

have partially diversified into other countries or sectors or, in a limited number of cases thus far, have had to cease

operations entirely. This section identifies both the financial and operational issues facing different areas of the

supply chain.

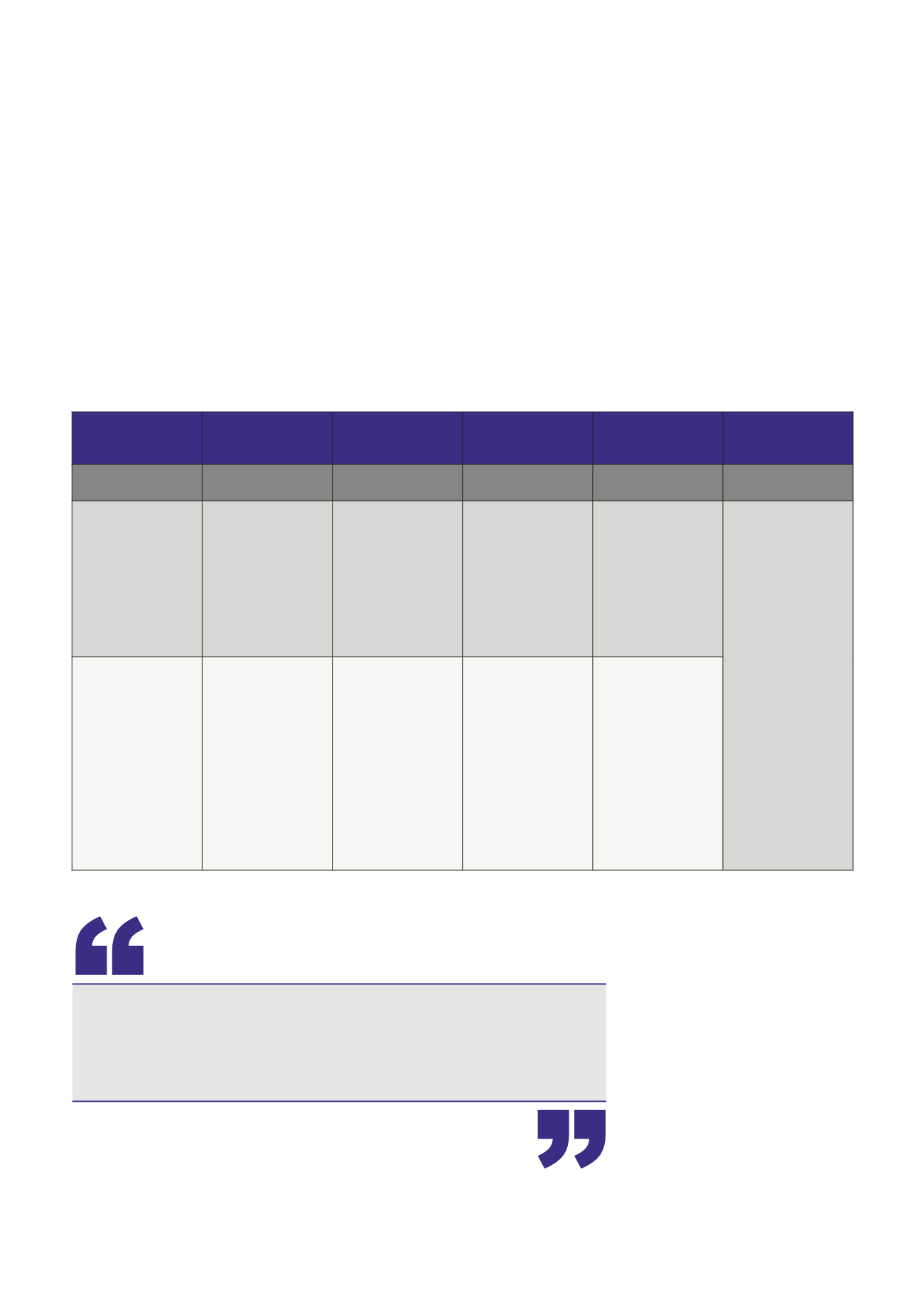

Figure 33: Supply Chain Categories and Sub-Sectors

Tier 1: E&P Companies

(End User)

Integrated Majors

Large/Small

Independents

Energy Utilities

Companies

Non-Operating

Companies

Exploration

Companies

Supply Chain

Categories

Reservoirs

Wells

Facilities

Marine and Subsea Support and Services

Tier 2:

Main contractors and

consultants

Â

Seismic data

acquisition

and processing

contractors

Â

Well services

contractors

Â

Drilling contractors

Â

Well engineering

consultants

Â

Engineering,

operation,

maintenance and

decommissioning

contractors

Â

Engineering

consultants

Â

Structure and

topside design and

fabrication

Â

Marine/subsea

contractors

Â

Heavy lift/pipelay

contractors

Â

Floating,

production, storage

units

Â

Catering/facility

management

Â

Sea/air transport

Â

Warehousing/

logistics

Â

Communications

Â

Recruitment

Â

Training

Â

Health, safety and

environmental

services

Â

Energy

consultancies

Â

IT hardware/

software

Tier 3:

Product and services

suppliers

Components

Sub-contractors

and sub-suppliers

Â

Geosciences

consultancies

Â

Data interpretation

consultancies

Â

Seismic

instrumentation

Â

Drilling and well

equipment design

and manufacture

Â

Laboratory services

Â

Machinery/

plant design and

manufacture

Â

Engineering support

contractors

Â

Specialist

engineering

services

Â

Specialist steels and

tubulars

Â

Inspection services

Â

Subsea manifold/

riser design and

manufacture

Â

Marine/subsea

equipment

Â

Subsea inspection

services

On average revenues across the supply chain

fell by 10 per cent in 2015, with a further fall

of 21 per cent forecast this year.