2 / 20

2 / 20

BIOPHYSICAL SOCIETY NEWSLETTER

2

JANUARY

2016

BIOPHYSICAL SOCIETY

Officers

President

Edward Egelman

President-Elect

Suzanne Scarlata

Past-President

Dorothy Beckett

Secretary

Frances Separovic

Treasurer

Paul Axelsen

Council

Olga Boudker

Ruth Heidelberger

Kalina Hristova

Juliette Lecomte

Amy Lee

Robert Nakamoto

Gabriela Popescu

Joseph D. Puglisi

Michael Pusch

Erin Sheets

Antoine van Oijen

Bonnie Wallace

Biophysical Journal

Leslie Loew

Editor-in-Chief

Society Office

Ro Kampman

Executive Officer

Newsletter

Catie Curry

Beth Staehle

Ray Wolfe

Production

Laura Phelan

Profile

Ellen Weiss

Public Affairs

Beth Staehle

Publisher's Forum

The

Biophysical Society Newsletter

(ISSN 0006-3495) is published

twelve times per year, January-

December, by the Biophysical

Society, 11400 Rockville Pike, Suite

800, Rockville, Maryland 20852.

Distributed to USA members

and other countries at no cost.

Canadian GST No. 898477062.

Postmaster: Send address changes

to Biophysical Society, 11400

Rockville Pike, Suite 800, Rockville,

MD 20852. Copyright © 2016 by

the Biophysical Society. Printed in

the United States of America.

All rights reserved.

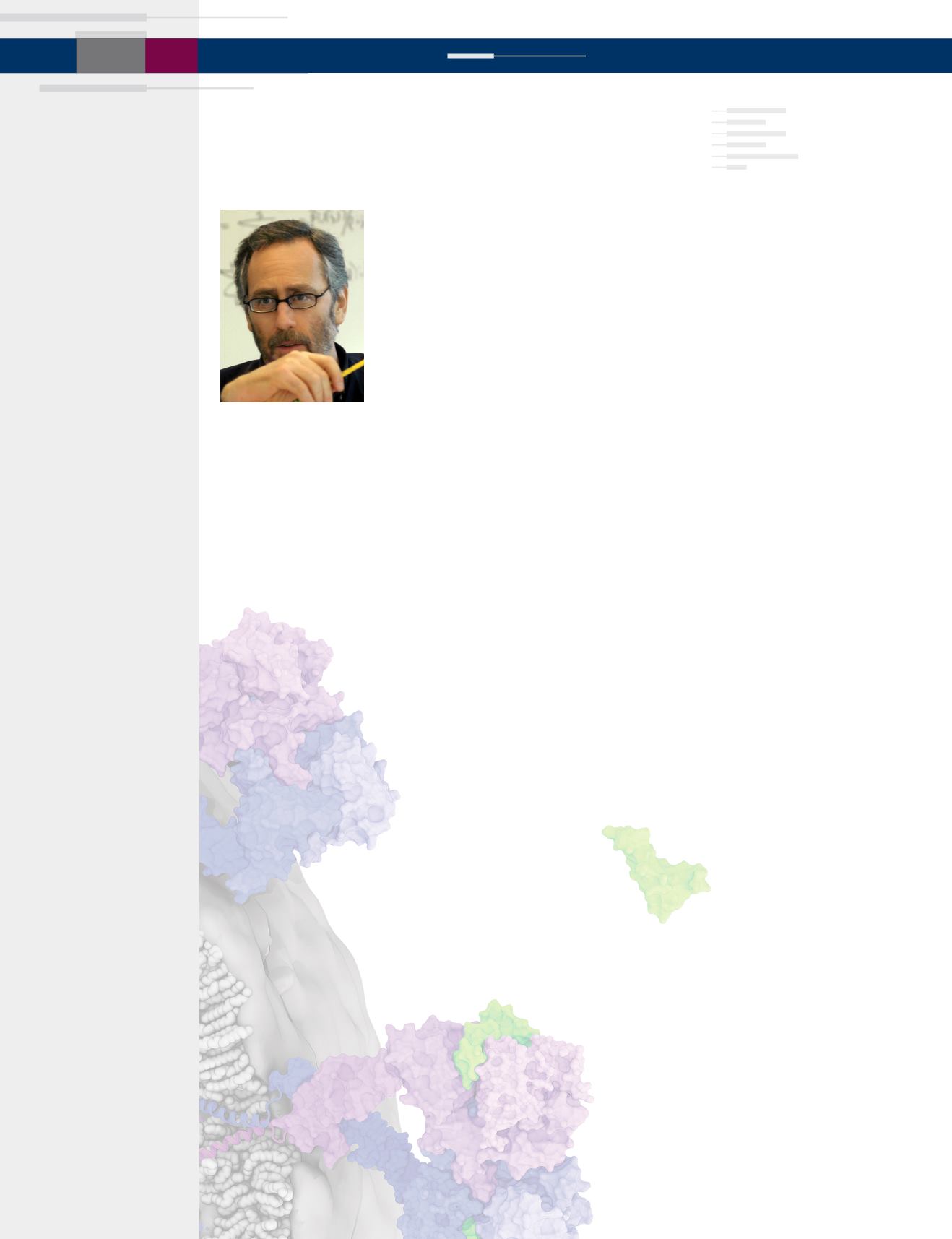

David E. Shaw

, Chief Scientist, D.E. Shaw Research, always believed that

he would work as a scientific researcher; he never imagined the unexpected

detour he would take into the world of finance, as a pioneer in quantita-

tive trading. Shaw’s father was a theoretical plasma physicist, his mother a

researcher in education, and his stepfather was an economist and professor

at the University of California, Los Angeles (UCLA). “I was raised in Los

Angeles, near UCLA, and my parents used to take me there so frequently

that it was some time before I learned the difference between a university and

a public park,” he recalls. “They looked pretty much the same to me, though

the university had a wider range of interesting things going on, and was

generally more entertaining.”

Shaw attended the University of California, San Diego, where he double-

majored in mathematics and in applied physics and information science.

He then earned his PhD from Stanford University in 1980. Shaw wrote a

doctoral dissertation that provided a theoretical framework for a new class of

computer architectures and algorithms that could be shown to offer asymp-

totically superior performance for certain mathematical operations related to

artificial intelligence and database management.

He joined the faculty of the Computer Science Department at Columbia

University, conducting research on the design of massively parallel special-

purpose supercomputers for various applications. “Although my thesis at

Stanford hadn’t involved the construction of any actual hardware,” Shaw

explains, “after arriving at Columbia, I received government funding to actu-

ally start building one of the weird supercomputers I’d designed on paper.”

The machine could not be constructed using standard components, so Shaw

and his students designed their own integrated circuits, and then connected

them to assemble a small-scale working prototype. They wrote code for the

machine that implemented some of Shaw’s algorithms. “We were thrilled

when the whole thing actually started working,” Shaw recalls.

Hooked on the idea of designing and building these special-purpose super-

computers, Shaw saw that building full-scale machines would require a much

larger budget than government grants could likely provide. He wrote a busi-

ness plan for a proposed startup venture that would manufacture massively

parallel supercomputers for commercial use, and began meeting with venture

capitalists.

It quickly became clear to Shaw that this venture would not take off, but in

the course of seeking funding, he had a chance meeting with executives from

Morgan Stanley that led him on a career detour. “The executives I met with

at Morgan Stanley told me that someone there had discovered a mathemati-

cal technique for identifying underpriced stocks,” Shaw says. “A group of

financial and technical people there had written some software that was using

this technique to make investment decisions on a fully automated basis, and

they were consistently earning an unusually high rate of return.” Shaw was

intrigued that they were using quantitative and computational methods in

the stock market, “and I couldn’t help wondering whether state of the art

methods that were being explored in academia could be used to discover

Biophysicist in Profile

DAVID E. SHAW