75 / 84

75 / 84

75

1

2

3

4

5

6

7

8

9

10

11

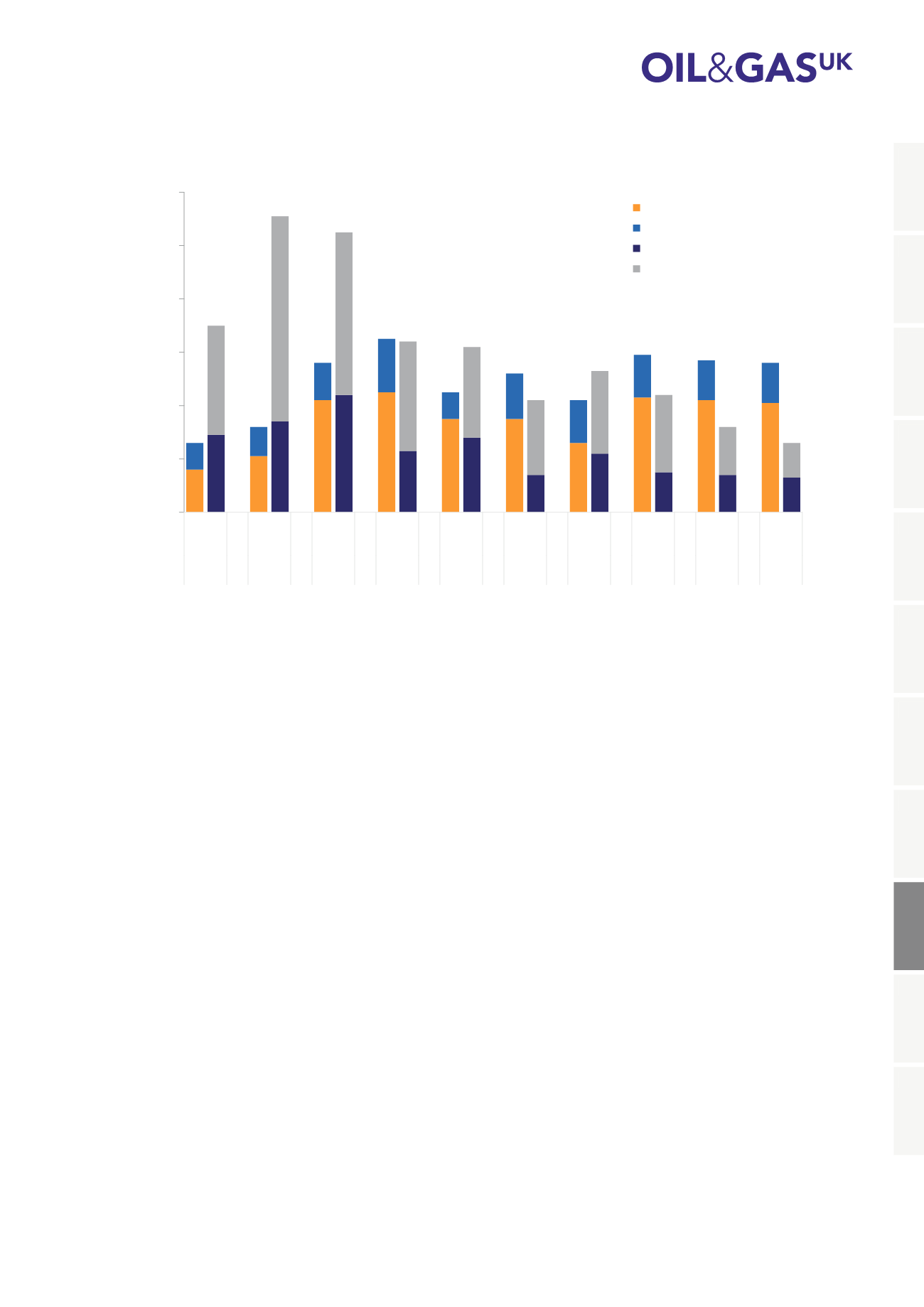

Figure 55: Exploration and Appraisal Activity

0

20

40

60

80

100

120

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

NCS

UKCS

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of Wells

NCS Exploration

NCS Appraisal

UKCS Exploration

UKCS Appraisal

Source: Common Data Access Limited, OGA, Norwegian Petroleum Directorate

Factors constraining exploration activity and success on the UKCS over the last five years have not been as

prominent in Norway. Access to finance is easier and more affordable due to the certainty provided by the

exploration tax credit (more detail below); there is not a perceived lack of prospectivity on the NCS as exploration

success has continued through maturity; and partner alignment is not as problematic due to more active state

involvement and fewer incumbent players.

Efforts have been made by the state over the past two years to stimulate exploration on the UKCS (see section 5.2

on drilling activity) but it will take several years for the full effects to be seen. The Norwegian state was quick to

act to incentivise exploration some 10 to 15 years earlier in response to declining activity during the early 2000s.

Coupled with the rising oil price during that period, the basin responded with an upturn in activity and some major

discoveries over recent years.

An example of early state intervention in Norway is the changes to the licence regime that have successfully

stimulated activity in mature and frontier regions. By making it simpler for new entrants to secure acreage

through licence awards and allowing them to buy and swap licence interests, there has been greater diversity and

a doubling in the number of companies operating on the NCS.

The annual system of Awards in Predefined Areas (APA), introduced in Norway in 2003, offers licences for large

areas close to existing and planned infrastructure to promote activity in mature regions. This is complemented

by a system of concession licence rounds held every second year that focus on under-explored frontier regions.

A further intervention by the Norwegian Government was an amendment to the Petroleum Tax Act adopted in

2004, known as the Exploration Tax Credit. This gave companies with a tax loss and no other production profits

the right to claim tax relief at the prevailing rate of 78 per cent on any exploration costs the year after they are

incurred. Financiers will typically allow companies to borrow against this credit, making funds for exploration far