18 / 84

18 / 84

ECONOMIC REPORT

2016

18

3.3 Carbon Markets and CO

2

Emissions

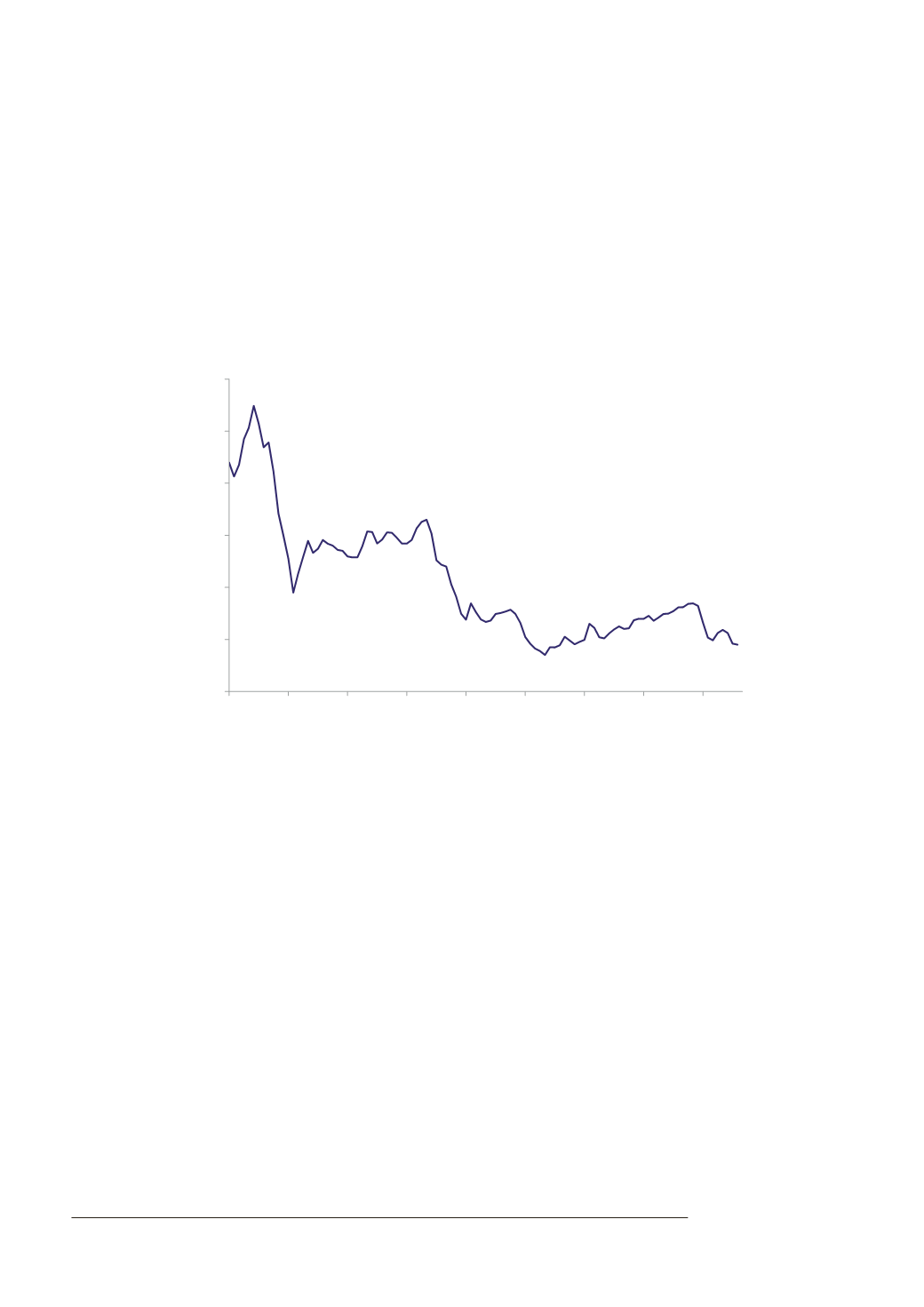

Phase III of the EU Emissions Trading Scheme (EU ETS) (2013-20) has beenmarked so far by a persistent large surplus

of emission allowances (EUAs) and depressed EUA prices. Market demand for allowances has been curtailed by

weak economic activity, rising renewables penetration and the continued auctioning of allowances by Member

States. Prices began a slow recovery in 2013 as the Eurozone crisis receded to reach €8/tonne (te) CO

2

in late 2015,

but the slump in energy prices in 2015-16 and the recent UK referendum vote to exit the EU have brought EUA

prices back below €5/te CO

2

.

Figure 7: Monthly Spot EUA (Carbon) Price

0

5

10

15

20

25

30

2008

2009

2010

2011

2012

2013

2014

2015

2016

EUA Spot Price (€/te CO

2

e)

Source: ICIS Heren, Intercontinental Exchange

Since the recession in 2008-09, ETS carbon prices

12

have not been high enough to induce switching to lower-carbon

fuels or to promote the intended investment in low-carbon energy sources. The steady expansion of renewables

(mainly wind, solar photovoltaics and biomass) across the EU since 2009 has been achieved through domestic subsidies

and other measures, not through EU-wide carbon pricing. In the UK, the switch from coal to gas in power generation

since 2013 has been accelerated through the UK’s own carbon price floor (CPF), which functions effectively as a

market-related tax, not through the ETS. The CPF continues to confer a competitive advantage for gas-fired generation

over coal but has now been capped at £18/te CO

2

(€22/te CO

2

) to prevent UK wholesale electricity prices from rising

further above those on the continent.

The shortcomings of the ETS have prompted EU efforts to reform the market through ‘backloading’ (reducing the

availability of allowances in later years) agreed in 2013 and the introduction of theMarket Stability Reserve (MSR) agreed

in 2015, which will take effect in 2019. These may, as intended, raise EUA prices towards the end of Phase III but it is the

current review of the EU ETS Directive, due to take effect in Phase IV (2021-30), that may be much more decisive.

The EU ETS remains ostensibly the central pillar of long-termEU decarbonisation policy. Finding a balance between the

interests of EU industries concerned about competitiveness and carbon leakage and the desire to deliver an effective

carbon price that changes behaviour will be the delicate task of EU legislators and Member States in late 2016 and

early 2017.

12

The amount that must be paid for the right to emit one tonne of CO

2

into the atmosphere.