41 / 60

41 / 60

page 41

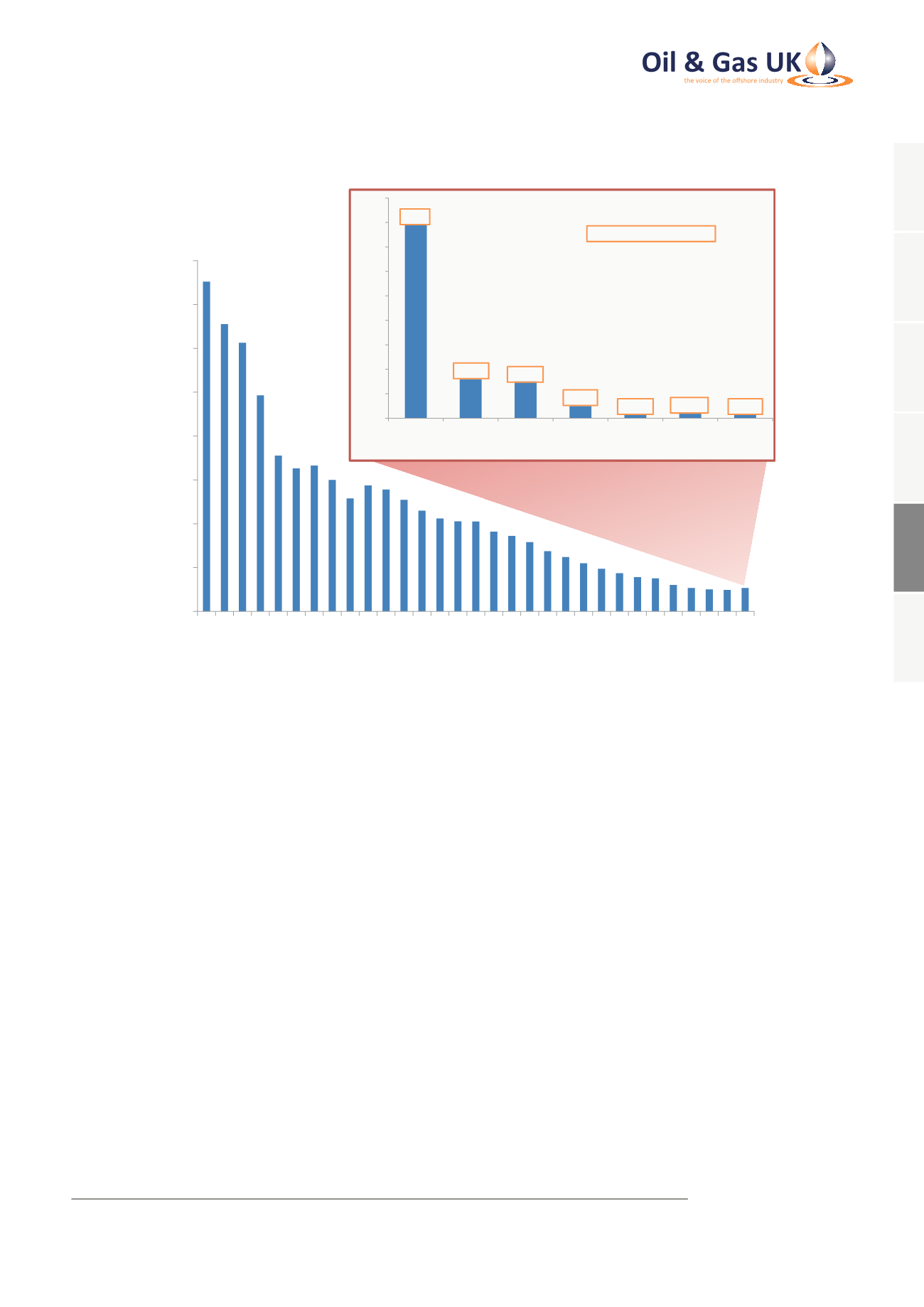

Figure 30: Average Production by Year per Field, with the Distribution of 2015 Fields

0

10

20

30

40

50

60

70

80

1985

1990

1995

2000

2005

2010

2015

Average Daily Production per Field (thousand boepd)

Source: Oil & Gas UK, Wood Mackenzie

0

20

40

60

80

100

120

140

160

180

<5,000 5,000 - 10,000 10,000 -

20,000

20,000 -

30,000

30,000 -

40,000

40,000 -

50,000

>50,000

Number of Fields

Daily Production (boepd)

1,600

46,000

32,000

23,000

14,000

7,000

91,000

Average Daily Production 2015

Production by Region

In 2015, the CNS accounted for 60 per cent of the total UKCS production. It is expected to remain the most

productive area over the next five years, but is forecast to reduce its share of UKCS output to around 45 per cent

by 2020.

Meanwhile, thewest of Shetland regionwill become increasingly important, with its proportion of UKCS production

rising from just 2.8 per cent in 2015 to around 20 per cent by 2020. This is the result of significant field start-ups,

such as Claire Ridge, Schiehallion, the Laggan-Tormore area and Solan.

The NNS region is forecast to hold up well through to 2020, with the decline in base production offset by significant

new field start-ups, including Mariner, Kraken and Western Isles. Production from the SNS will continue to decline

over time and it is estimated that over half of the fields in this region are due to cease production by 2020. As in

other areas of the UKCS, there is potential for output to be boosted by new field start-ups. Securing development

of the Tolmount field

15

and the performance of the Cygnus field

16

will be crucial beyond 2020. These two fields

alone could be producing over one-third of SNS volumes by the early part of the next decade.

Production from the UKCS is highly reliant on a network of ageing, complex and interdependent infrastructure.

Careful management of this infrastructure is crucial as removal, which for some fields is now a real threat, would

have a severe impact on production, causing volumes to be permanently lost. Innovative solutions must be found

to overcome access to infrastructure issues to ensure fields are not prematurely decommissioned.

15

http://bit.ly/EONtolmountdiscovery16

www.engie-ep.co.uk/our-operations/cygnus.aspx1

2

3

4

5

6