108 / 122

108 / 122

108 |

Southern Corridor GRIP 2017–2026

20–40%

<20%

<40%

10–30%

>20%

0–50GWh/d

0–80% of capacity

50–250GWh/d

250–600GWh/d

600–1100GWh/d

>1100GWh/d

<30%

80–99% of capacity

99–100% of capacity

20–40%

<20%

<40%

10–30%

>20%

0–50GWh/d

0–80% of capacity

50–250GWh/d

250–600GWh/d

600–1100GWh/d

>1100GWh/d

<30%

80–99% of capacity

99–100% of capacity

20–40%

<20%

<40%

10–30%

>20%

0–50GWh/d

0–80% of capacity

50–250GWh/d

250–600GWh/d

600–1100GWh/d

>1100GWh/d

<30%

80–99% of capacity

99–100% of capacity

20–40%

<20%

<40%

10–30%

>20%

0–50GWh/d

0–80% of capacity

50–250GWh/d

250–600GWh/d

600–1100GWh/d

>1100GWh/d

<30%

80–99% of capacity

99–100% of capacity

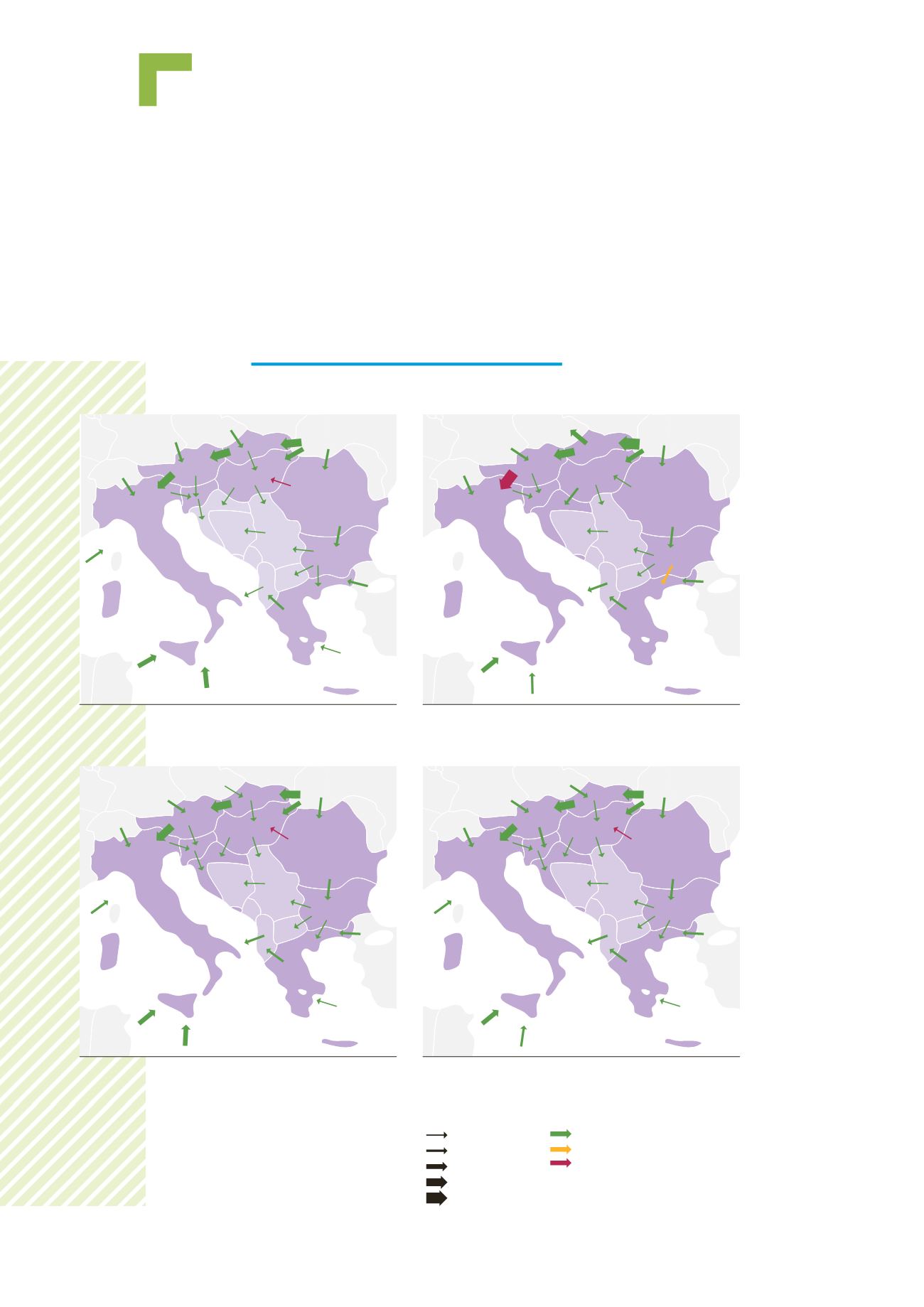

Figure 7.4.1:

2020 Low Reference

Figure 7.4.3:

2020 Low AZ max

Figure 7.4.2:

2020 low RU max

Figure 7.4.4:

2020 Low LNG max

7.4 Flows response to price

signals

In this paragraph we examine how the flows in the Region are changed when the

supply source prices are modified with reference to the reference case. The gas

sources examined are Russia, LNG and Azerbaijan. The price of one source at a

time is reduced by 10% and the flows are recalculated by the ENTSOG NeMo tool

which minimises the overall EU gas bill. The results are presented for the two

infrastructure levels (Low and PCI) and the two points in time (2020 and 2030).

7.4.1 LOW INFRASTRUCTURE CASE

Legend

20–40%

<20%

<40%

10–30%

>20%

0–50GWh/d

0–80% of capacity

50–250GWh/d

250–600GWh/d

600–1100GWh/d

>1100GWh/d

<30%

80–99% of capacity

99–100% of capacity